Apple And ASUS Big Winners As PC Shipments Gather Momentum

Market research firms International Data Corporation (IDC) and Canalys are in agreement that the global PC market continues to recover, with the former highlighting a 3% uptick in year-over-year shipments to 64.9 million units, and the latter counting 62.8 million shipments for a 3.4% growth rate compared to last year. Where they're not in agreement, however, is which PC maker benefited the most compared to last year.

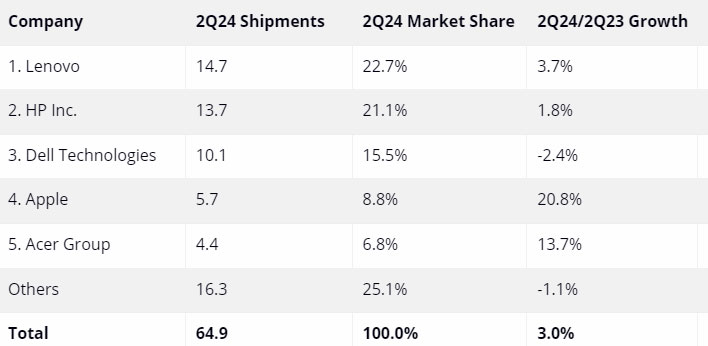

There are different ways to analyze this. If looking at the market share leaders, IDC has Lenovo on top with 14.7 million second-quarter shipments for a 22.7% share of the market, followed by HP (13.7 million shipments for a 21.1% share), Dell (10.1 million shipments for a 15.5% share), Apple (5.7 million shipments for an 8.8% share), and Acer (4.4 million shipments for a 6.8% share). After the top five, the market research firms clumps the rest into an "Others" category with a combined 16.3 million second-quarter shipments for a 25.1% share.

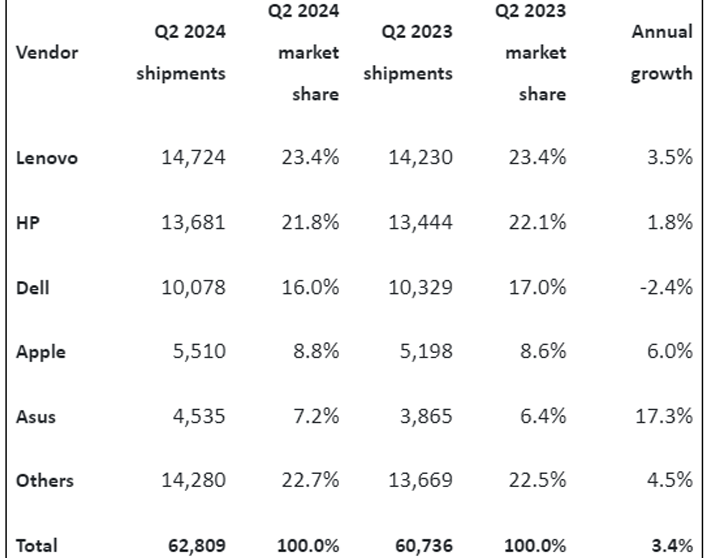

The shipment auditing by Canalys saw the same ranking among the top four, with Lenovo at the top spot (14.7 million shipments, 23.4% share), followed by HP (13.7 million shipments, 21.8%), Dell (10.1 million shipments, 16% share), and Apple (5.5 million shipments, 8.8% share).

Those are slightly rounded figures, with the breakdowns of the top four players being nearly identical. Where they differ is how ASUS factors into the equation. IDC makes no mention of ASUS, while Canalys has the PC maker settling into the number five spot with 4.5 million shipments and a 7.2% share.

While there's a big gap between ASUS and major OEMs like Lenovo and HP, the annual growth rate is unrivaled—Canalys says ASUS saw a staggering 17.3% annual growth rate. The next closest was Apple at 6%, followed by Lenovo at 3.5% and HP at 1.8%. Dell, meanwhile, saw its annual growth rate dip by -2.4%.

Likewise, IDC shared similar annual growth rate figures for the big three (3.7% for Lenovo, 1.8% for HP, and -2.4% for Dell), but it claims Apple's saw a massive 20.8% growth, followed by Acer at 13.7%. The "Others" group where ASUS presumably falls into collectively saw a -1.1% decline.

Make of all that what you will, but if viewing both reports under the same lens, Apple and ASUS are the big winners, in terms of growth rate. Apple's rise is especially interesting, given that it's the only exclusively non-x86 player on the list. It also suggests that the market could be in for an interesting showdown between Apple's Macs and Arm-based Copilot+ PCs based on Qualcomm's Snapdragon X Elite and Plus hardware, as the AI arms race heats up.

"In recent months, most of the industry players have laid out their initial strategies for AI PCs focusing primarily on the component side and the potential of the commercial market. While IDC believes the commercial market has the biggest short-term upside for AI in the PC industry, the consumer story has yet to be told in full," IDC says. "All eyes are on Apple to drive that message later this year with anticipated product launches, but it shouldn't be overlooked that Qualcomm, Intel, and AMD are all likely to make noise around both consumer and commercial AI PCs."

Likewise, Canalys notes that the market turnaround is happening as AI PC roadmaps come to fruition.

“The quarter culminated with the launch of the first Copilot+ PCs powered by Snapdragon processors and more clarity around Apple’s AI strategy with the announcement of the Apple Intelligence suite of features for Mac, iPad and iPhone. Beyond these innovations, the market will start to benefit even more from its biggest tailwind - a ramp-up in PC demand driven by the Windows 11 refresh cycle," Canalys states in its shipment report.

Buckle up, it's going to be an interesting year that could see some significant movement among the top players. In the meantime, you can check out the latest shipment reports from IDC and Canalys for a deeper